Current vs. Noncurrent Digital Assets

How to appropriately present digital assets on the Company's balance sheets?

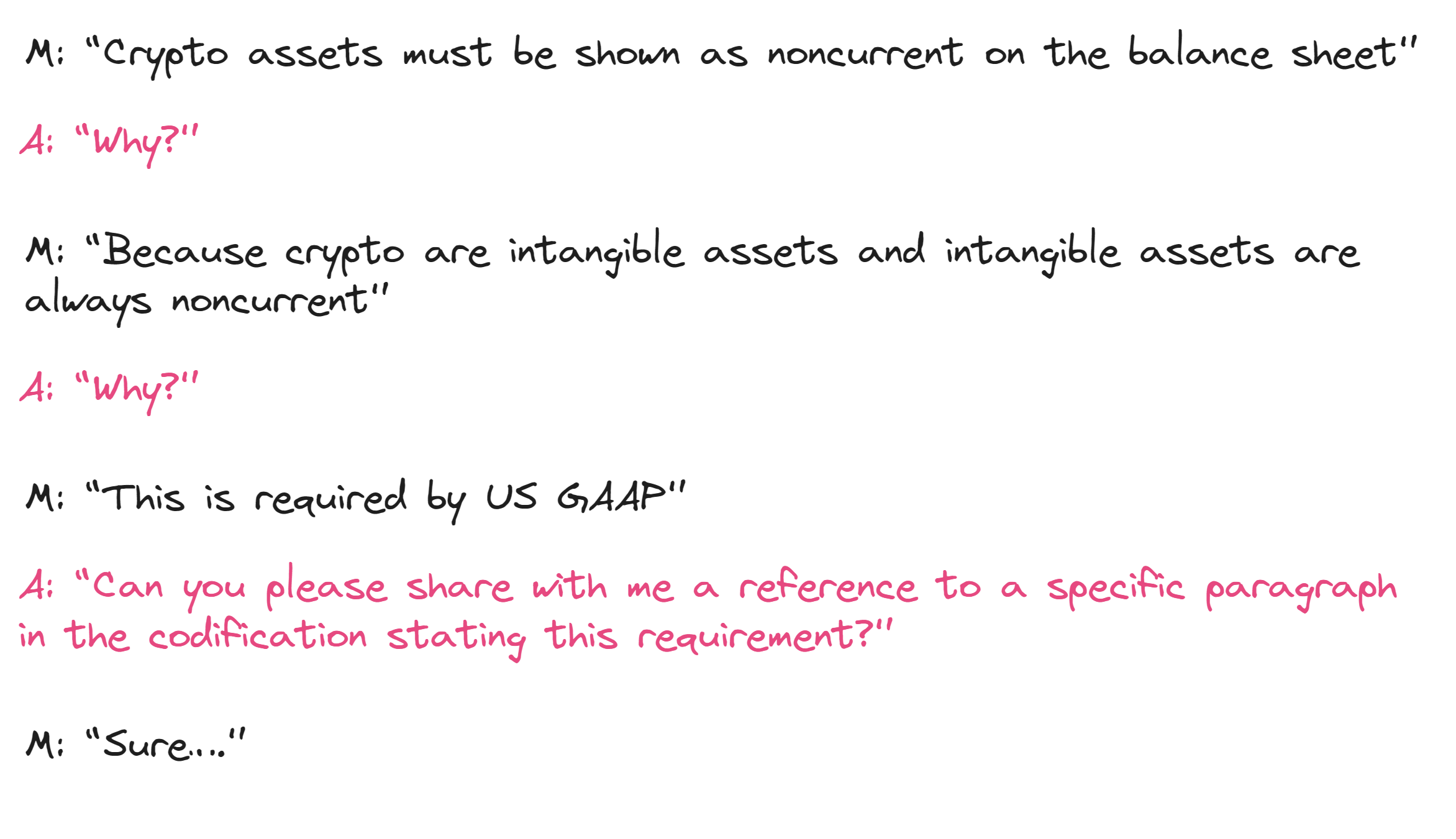

Chat with a Sr. Audit Manager from Withum, July 2023:

I never heard back from Withum after this. This time, I decided to adopt an empirical approach to the question. Here are the most well-known listed U.S. companies primarily engaged in the cryptocurrency business, segregated based on how management presents general digital assets on their balance sheet:

First, I wanted to note that in our sample, there are two mixed cases - Coinbase Global Inc. and BTCS Inc. Both companies disaggregate digital assets into several line items (i.e., generic vs. special categories of digital assets) and present special categories of digital assets differently from generic digital assets:

Coinbase Global classifies the generic digital assets category ('Crypto assets held') as noncurrent assets. In contrast, 'USDC' and 'Customer crypto assets' are presented as current assets.

BTCS Inc. presents the generic digital assets category ('Crypto assets' or non-staked crypto assets) as current assets. 'Staked crypto assets' are presented as non-current assets if they are staked and locked up for over one year. The remainder is shown as current assets.

Ault Alliance Inc., Marathon Digital Holdings, Inc., Core Scientific, Inc., and Riot Platforms, Inc. classify crypto assets as current assets.

Unicoin classifies digital assets as noncurrent assets.

Based on what we’ve seen so far, it seems that the majority of companies operating in crypto present digital assets as current assets. Is it the correct answer?

Existing guidance on the classification of current vs. noncurrent assets is not as clear and consistent as one might hope. The section “Classification of Current Assets” in the accounting standards codification by FASB limits the discussion to a list of items that should generally be classified as current items [FASB ASC 210-10-45-1] and another list consisting of items that generally are not appropriate to classify as current assets [FASB ASC 210-10-45-4]. This is not particularly useful. At least, the classified balance sheet is not a requirement, and companies can always elect not to categorize assets and liabilities between current and noncurrent categories [FASB ASC 210-10-15-3].

FASB ASC 210-10-45-2 states that the segregation of current assets from noncurrent should be based on the longer of two:

a) one-year time period; and

b) operating cycle.

How exactly do we apply the longer of these two periods when assessing whether assets are current or noncurrent for financial reporting purposes? The only phrase that can be interpreted as an answer comes from the FASB Master Glossary definition of Current Assets: “Current assets is used to designate cash and other assets or resources commonly identified as those that are reasonably expected to be realized in cash or sold or consumed during the normal operating cycle of the business…”.

Based on this definition, one might conclude that the criterion for segregating current and noncurrent assets is the expected period of the conversion of assets (whether it is longer or shorter than twelve months).

Intention is key. But what if you know that the door is heavy and will take a long time to open? In this case, intention alone is not sufficient. The intention should be supported by expectations grounded in the multiverse of relevant facts and circumstances.

As with any concept of a multiverse, if you search long enough, you can find an arrangement of facts and circumstances that supports any position. However, more often than not, I noted the following to be true:

Crypto-native businesses' digital assets are typically used in operations to settle current obligations and thus serve as a means of exchange. Under these circumstances, the presentation of digital assets as current assets is more appropriate.

Businesses other than crypto-native ones typically hold digital assets as investments to benefit from appreciation. Under these circumstances (unless the company plans to sell these assets in the next 12 months), the presentation of digital assets as noncurrent assets is more appropriate.

Therefore, our view here is that, in general, digital assets should be presented as current assets if the intended use and availability of funds indicate that digital assets may be converted into cash for operations within the next 12 months or used in the cashless settlement of existing current obligations.