Opinionated Guide on Financial Statement Formatting

This guide provides answers to the most common questions that preparers of financial statements encounter in practice. Consistency, clarity, and professional appearance.

CPE Flow

CPE Flow Annual Membership Plan

Annual membership at CPE Flow is designed to provide you with an all-access pass to the entire library of cutting-edge CPE courses and resources tailored to your continuing professional education needs.

This guide does not reflect any financial reporting framework requirements. The only goal of this post is to share some of the practices observed in the past. However, when I believe that a better way of presentation exists, I suggest this “better” way and ignore the approaches followed by most of the other practitioners.

1. Textual Data.

1.1. Font Family.

Use the Inter, Arial, or Times New Roman font family for readability.

1.2. Font Size.

For titles, use a font size of 16-point, bold.

For section headings, use 14-point bold.

For subheadings, use 14-point italic.

For body text, use 12-point regular.

For footnotes, use 10-point regular.

1.3. Characters and symbols.

Use the Unicode Latin character set.

Within the text, spell out “percent” instead of using the “%” symbol in all cases except numerical percentages, which should be followed by “%”.

In tables, place currency symbols (e.g., $, €, £) only at the top and bottom of columns.

In tables, use of percentage (%) signs on each line where applicable.

If the reporting currency is Canadian Dollars, in the introductory note, specify: "All figures are in Canadian dollars (CAD)." After that, use C$ throughout the report to avoid confusion with US dollars. For narrative or footnotes, you can use CAD when needed, but C$ in tables is the most professional choice.

2. Capitalization

In sub-headings capitalize the first word and proper nouns. Do not capitalize articles, prepositions, and “to” preceding an infinitive.

Don't capitalize currencies: U.S. dollar instead of U.S. Dollar; Canadian dollar instead of Canadian Dollar.

Always capitalize department names.

Employee titles are only capitalized when they appear immediately before the employee’s name.

Within headers, the name of the report should be in the proper case

Within headers, the Company name should be capitalized.

3. Margins and Spacing

Set the left margin to 1.5 inches and all other margins to 1-inch margins for both print and digital formats.

Use 1.15 line spacing for body text

Use single-line spacing for endnotes

Leave a single blank line before and after each table or section heading

4. Alignment

Generally, avoid indentation for block paragraphs.

Left-align all text and explanations

Right-align all numeric data in tables to allow for easy comparison across rows

Right-align page numbers in the footer

Section headers should be center-aligned

5. Grammar

Use adjectives with nouns.

Use only pronouns in a 3rd party form. However, you may use first person for direct company references, like "We at XYZ Company ensure accuracy."

Use numerals for all numbers.

6. Spelling

US vs. U.S.: Use "U.S." when referring to U.S. GAAP.

“Non…” terms: Accounting terms starting with “non” like “noncash”, “noncurrent”, etc., should be spelled as single words (without a hyphen).

Proforma vs. Pro-forma: Use `Proforma`.

Refer to quarters as `X quarter of 20XX`

Use numerals for all numbers.

When relevant, include the valuation method by adding after the noun `at Cost` or `at Fair Value`.

Use “…, Beginning Balance” or “…, Ending Balance” for roll forwards.

Use short names for second and subsequent references to a person or company.

List each reference to an authoritative source individually: `ASC 606-10-25-1(a), ASC 606-10-25-1(d)` instead of `ASC 606-10-25-1(a,d)`

7. Punctuation

Use the serial comma before the final “and” in a series of three or more items and after each item, including the penultimate item.

Always use periods at the end of bulleted items that are complete sentences

End each sentence with a period.

Use hyphens to clarify nouns, such as year-end adjustments.

Apply hyphens in adjectival phrases like income-tax expense or long-term liabilities. Clarify meaning in cases of repeated terms, such as re-assess (assess again) versus reassess (standard review). Use hyphens with proper nouns, e.g., non-GAAP disclosures or anti-FASB criticism.

Use hyphens to prevent awkward doubling of vowels, such as in de-escalating risk exposure or pre-existing contractual obligations. However, avoid hyphens with prefixes like re, co, and pre, which should remain solid, as in reevaluating accounting policies or preapproving related-party transactions.

Hyphenate numerical figures, as in mid-2023 guidance or three-year rolling average.

Do not use parenthesis to indicate the negative values. Always list the positive value first, ensuring clarity: Increase (Decrease) is correct, while Decrease (Increase) or (Decrease) Increase is not.

Use spaces before parentheses, e.g., Revenue (Expense), and avoid slashes like Profit/Loss.

2. Numerical Data

Negative amounts should be shown in parentheses.

Zero should be shown as `-`.

Use rounding to the nearest thousand for most financial figures based on the level of materiality. Typically, figures are rounded to the nearest thousand or million, depending on the magnitude of the numbers being reported.

Within the same disclosure, you can use multiple denominations for numbers of different magnitude and order (e.g., debt vs. interest) as long as you specify the units clearly for each figure (e.g., C$5.75 billion for debt, C$500,000 for interest)

When necessary, financial tables may use two decimal points (e.g., for earnings per share). Ensure consistent use of two decimal places for percentages e.g., 2.75%) across all statements.'

Clearly state the rounding convention at the top of each financial table header and be consistent within each table. For example, In Thousands [of CAD], Except Weighted-Average Remaining Lease Term in Years.

For the use of currency symbols and reporting currency see 1.1.3.

Start the denomination statements from the rounding degree (followed by the reporting currency only when it differs from U.S. Dollars):

`In billions` or `In Billions Canadian Dollars`

`In millions` or `In Millions Canadian Dollars`

`In thousands` or `In Thousands Canadian Dollars`

`In U.S. Dollars` or `In Canadian Dollars`

Additionally, the denomination statement may be continued with the following report-specific wording:

Income Statement: `, except the number of shares which are reflected in thousands and per share amounts` or `, Except Per Share Amounts`

Balance Sheets: `, except the number of shares which are reflected in thousands and par value` or `, Except Par Value`

Numbers in the range [1-9] may be spelled out with letters instead of numbers.

3. Tabular Data

Tables should be full page width, with clear borders separating rows

Keep empty spaces between columns

The respective year number should be in the header row in bold with a single underline.

Numeric data should always be right-aligned, and text labels left-aligned

Use light shading to distinguish between rows

Use a single line above subtotals and a double line below totals

For the use of percentage and currency symbols, see section 1.1.3.

4. Structure, Layout, and Organization

4.1 Document Structure

The title page should include the company name, the document title (e.g., Annual Financial Statements), and the reporting period (e.g., For the Year Ended December 31, 2024). For example, "XYZ Corp. Financial Statements for the Year Ended December 31, 2024"

Include a detailed table of contents that lists all sections and sub-sections with page numbers. A table of contents should be placed after the title page but before any financial statements.

Within the content table, list all the footnotes under Notes to the Financial Statements.

Within the content table, use leader dots to guide the reader from the section title to the page number.

Add a glossary section at the end of the report.

Place all appendices at the end of the report. Appendices should be logically grouped and referenced within the main document as needed.

The order of financial statements depends on the interest of primary users of financial statements. We generally recommend the following ordering:

Accountant report,

Income statements,

Balance sheets,

Cash flow statement,

Statements of changes in equity, and

Footnotes.

4.2 Page Structure

Start major sections (each of the main financial statements) on a new page.

Avoid splitting tables across pages. If a split is necessary, repeat the table headers on the new page.

The page header should be included on the first page of each report section only. All footnotes are considered a single report section for this determination.

The page footer should be positioned in the center of each page.

The footer of each page other than in the “Accountant’s report” section should contain the statement "See accompanying Notes to Consolidated Financial Statements".

The footer should also contain the following second line:

`Company Name | Year Report Form | Page number.`

4.3. References and Hyperlinks

Use hyperlinks in digital reports for external data.

Use hyperlinks in digital reports for different sections of the same document.

Use full references in footnotes or appendices for printed versions.

When presenting digital reports, include hyperlinks in the main text to navigate directly to the relevant appendix sections.

5. Financial Statement Structure

5.1. Balance Sheet

Use bold for major headings like Total Assets and Total Liabilities.

Include subtotals for both current and non-current assets as well as the grand total for assets.

5.2. Income Statement

Total Revenue and Gross Margin are presented as clear subtotals in the Income Statement, while similar subtotals for other key sections, such as Total Operating Expenses or Total Other Income/Expense, are omitted. Including these subtotals consistently would provide a more cohesive presentation, making it easier to follow the flow of income and expenses.

Present Revenues with a breakdown of line items into product and service revenues. Present the Cost of revenue from product sales separately from the cost of service revenues. Providing a consistent level of detail across all major income and expense categories enhances clarity.

When only losses are presented in each of the periods in subtotals in the Income Statement, such as Other Comprehensive Income (Loss), the line item should be named Other Comprehensive Loss, with all figures on this line presented in parenthesis.

When only net gains are presented in each of the periods in subtotals in the Income Statement such as Other Comprehensive Income (Loss), the line item should be named Other Comprehensive Income with all figures on this line presented as positive numbers.

Show the following numbers as positive numbers when the account balance is in the default position for the group of accounts. The default position for the group of accounts is:

Revenue accounts have a default position of credit.

Cost of revenue accounts have a default position of debit.

Selling, general, and administrative expense accounts have a default position of debit.

Interest income/(expense) accounts have a default position of credit.

Other income/(expense) accounts have a default position of credit.

Income tax provision accounts have a default position of debit.

All other accounts (below the operating profit line item) have a default position of credit regardless of whether they represent income or expense (this means that credit balances are presented as positive and debit balances as negative).

Gross, operating, pre-tax, net income and other form subtotals that consist of multiple groups of accounts identified above have a default position of credit.

5.3. Cash Flow Statement

Each of the 6 main sections of the report should be preceded by the name of the respective section:

operating cash flows,

finance cash flows,

inesting cash flow,

effect of exchange rate changes,

net increase (decrease) in cash and cash equivalents,

and supplemental cash flow information.

Main section headers should be in bold, with no indentation:

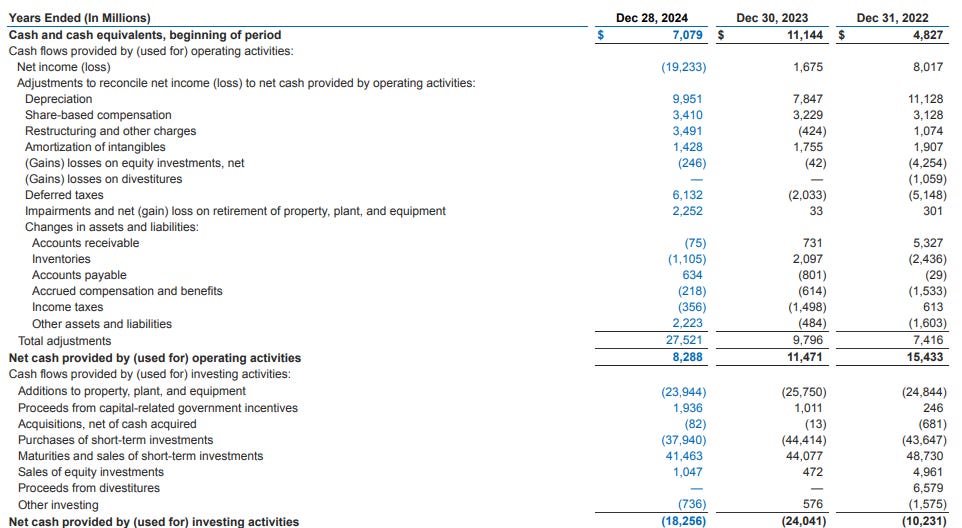

Intel Form 10-K 2024 Section subtotal lines such as “Net cash provided by operating activities” should be in a bold variation, with no indentation.

First-level activity line items are included only in the operating cash flows section when the indirect method of preparation of cash flows is used. In this scenario, the following three lines should be written using regular (not bold) font variation, and single indentation:

Working capital provided by operations is calculated as the sum of:

Net income

Adjustments to reconcile net income to cash generated by operations:

expenses with no effect on working capital

nonoperating losses/(gains)

Changes in {non-cash working capital}/{operating assets and liabilities}.

Second-level nested line items (common within operating activities under "Changes in operating assets and liabilities") should be in regular (not bold) variation, double indented, and used for:

Items nested in the first-level activity in the operating cash flows

Any items listed in the investing and financing cash flows.

Third-level nested rows (rare, but may appear under grouped changes like “Other assets and liabilities”) should be in sentence case, regular (not bold) variation, and indented three levels if used.

“Cash and cash equivalents, beginning of period” and “Cash and cash equivalents, end of period” should be in regular font (not bold), and with no indentation.

BTCS Form 10-K 2024 Supplemental disclosure lines such as “Cash paid for interest” or “Non-cash investing and financing activities” should be in regular (not bold) font, and double-indented:

Apple Inc. Form 10-K 2024 When using the indirect method, operating cash flows should be broken into:

working capital provided by operations, calculated as:

net income

expenses with no effect on working capital

nonoperating losses/(gains)

changes in non-cash working capital.

Non-cash transactions should be presented in a separate table following the cash flow statement.

References to the income statement subtotals should use the same wording as in the income statement. Examples include Net Income referenced Cash Flow Statement and Statement of Changes in Equity.

Direct cash inflows/(outflows) should be presented as the line item that contains Proceeds/(Payments).

Indirect net components of operating cash flows should be presented as the line items that contain “Increase/(Decrease)” or “From/(Used In)”.

5.4. Statement of Changes in Equity

Present movements in each equity component (e.g., common stock, retained earnings) separately.

Clearly state each separate class of shares.

Ensure that the names of the line items carried from the Balance Sheet and Income Statement match the names of the same items in the source reports.

5.5. Footnote Disclosures

Footnote disclosures should be presented as distinct, sequentially numbered sections.

The order of footnote disclosures should correspond to the relevant line items in the financial statements.

Footnote disclosures should be separated by a line break or sufficient white space.

Use indentation for subsections.

Split the content of longer disclosures into paragraphs.

Use indentation to differentiate between topics, especially when providing detailed notes on accounting policies.

Bullet points or numbered lists can be used:

(a) when discussing multiple items,

(b) to break down complex information, or

(c) to separate dense blocks of text.

6. Electronic Format Guidelines

This section covers the final formatting and file submission standards to ensure uniformity across digital and printed formats.

6.1 PDF Standards and Consistency Checks

Use PDF format to ensure consistent formatting across different platforms.

Always check the final PDF to ensure that page breaks and formatting are preserved correctly.

Verify that all tables are displayed in full and that no data has been cut off during the conversion process.

6.2 File Naming Conventions and Version Control

Use standardized file names like `Company_Q3_FY2024_FS_v5_101524.pdf` for easy identification.

Include the company name, year, and report type in the file name.

For version control, include a version number and the date it was prepared in the file properties or at the bottom of the document to ensure updates are tracked.

Conclusion

The public needs companies to produce financial statements that are prepared with clarity, professionalism, and consistency. This guide was intended to assist preparers in handling common formatting questions to help them make sure that their product of work meets these requirements. However, we highlight that this is only the first version of the guide, and many questions may not have been reflected here. If you have relevant topics and/or questions that should be added to this guide, please feel free to reach out to us at info@techaccountingpro.com