Accounting for Tether (USDT)

Let's analyze whether USDT is a financial asset or not

On March 18, 2024, Mega Matrix Corp., filed with the SEC, Form 10-K that included the following narrative:

“Reclassification of digital assets and stablecoins. As Tether reserves the right under its user agreement to redeem USDT by in-kind redemptions of other assets it holds in its reserves and as Tether has held precious metals and other non-financial assets in its reserves, it does not appear that USDT meets the definition of a financial instrument under ASC 825-10-20. The Company reclassified USDT, amounting $90,100 as of December 31, 2022, from stable coins to digital assets. The reclassification had no impact on net assets as of December 31, 2022, and revenues and net loss for the year ended December 31, 2022.”

[Excerpt from Form 10-K filed by Mega Matrix Corp. on March 18, 2024]

Today, we will try to take another look at accounting for USDT and learn more about what challenges the current definition of a financial instrument creates.

USDT is commonly accounted for as financial assets in a manner similar to USDC. This accounting has been rooted in the treatment of USDC that was first described in Coinbase’s financial statements:

“USDC is a stablecoin redeemable on a one-to-one basis for U.S. dollars. USDC is accounted for as a financial instrument on the consolidated balance sheets.”

[Excerpt from Form 10-K of Coinbase Global, Inc.]

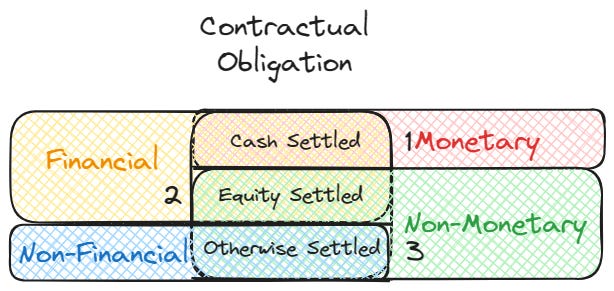

In order to answer whether it is appropriate to account for USDT under the same model as USDC, we need to understand what is the financial instrument. To find out, we will try to take a look at the definition given in the current accounting standards codification by FASB. The codification defines the financial instrument as follows:

Cash, evidence of an ownership interest in an entity, or a contract that both:

a. Imposes on one entity a contractual obligation either:

To deliver cash or another financial instrument to a second entity

To exchange other financial instruments on potentially unfavorable terms with the second entity.

b. Conveys to that second entity a contractual right either:

To receive cash or another financial instrument from the first entity

To exchange other financial instruments on potentially favorable terms with the first entity.

The use of the term financial instrument in this definition is recursive (because the term financial instrument is included in it), though it is not circular. The definition requires a chain of contractual obligations that ends with the delivery of cash or an ownership interest in an entity. Any number of obligations to deliver financial instruments can be links in a chain that qualifies a particular contract as a financial instrument.

Contractual rights and contractual obligations encompass both those that are conditioned on the occurrence of a specified event and those that are not. All contractual rights (contractual obligations) that are financial instruments meet the definition of asset (liability) set forth in FASB Concepts Statement No. 6, Elements of Financial Statements, although some may not be recognized as assets (liabilities) in financial statements—that is, they may be off-balance-sheet—because they fail to meet some other criterion for recognition.

For some financial instruments, the right is held by or the obligation is due from (or the obligation is owed to or by) a group of entities rather than a single entity.

[Excerpt from FASB ASC Glossary]

As noted above, any chain of contractual obligations that ends with the delivery of cash or an ownership interest in an entity falls under the category of financial instruments. Further, another significant idea (also highlighted with bold in the excerpt above) is that obligation within the chain may be conditioned on the occurrence of a specified event. It may be interpreted in different ways, but the presence of a single realistic scenario where an obligation is being settled in cash would generally be sufficient to classify such an obligation as a financial instrument.

Let’s provide a specific example and it will be a relatively simple one. Under US GAAP, the accounting for advance payments denominated in foreign currency depends on whether the advance payment is refundable or not.

Refundable deposits and advances (both amounts received from customers and a amounts paid to suppliers) are monetary liabilities and assets. Therefore, if the amounts are refundable in a foreign currency, the recognized asset or liability must be remeasured in the functional currency on each reporting date at the current exchange rate.

[Excerpt from “Deloitte’s Roadmap: Foreign Currency Matters” by Deloitte]

Based on the above guidance, refundable advance payments are treated as monetary assets and are remeasured based on changes in the exchange rate of the foreign currency. Non-refundable payments are measured using the exchange rate that existed as of the date when the advance was made. This guidance gives us one example of the situation when a realistic scenario of cash settlement affects accounting for the asset.

Now, one additional note that we need to make here, is regarding whether the monetary assets are financial instruments or not. And here is a piece from EY that helps us to answer this question:

“It should be noted that the terms “financial assets” and “monetary assets” are not synonymous. For example, an investment in common stock is a financial asset but is not a monetary asset.”

[Excerpt from the Guide “Nonmonetary Transactions” by EY]

I summarized the main idea in the following chart:

Based on this analogy, we can deduce that the presence of a scenario where the obligation is settled in cash may be sufficient to account for an obligation as a financial instrument. Will we be able to apply this criterion to USDT? Let’s take a look at the documents that contain Tether’s terms.

About Tether Tokens; General Restrictions; Forks: Tether issues and redeems Tether Tokens. Tether Tokens may be used, kept, or exchanged online wherever parties are willing to accept Tether Tokens. Tether Tokens are 100% backed by by Tether’s Reserves. Tether Tokens are denominated in a range of Fiat. For example, if you purchase EURT, your Tether Tokens are 1-to-1 pegged to Euros. If you cause to be issued EURT 100.00, Tether holds Reserves valued at €100.00 to back those Tether Tokens. The composition of the Reserves used to back Tether Tokens is within the sole control and at the sole and absolute discretion of Tether. Tether Tokens are backed by Tether’s Reserves, including Fiat, but Tether Tokens are not Fiat themselves. Tether will not issue Tether Tokens for consideration consisting of the Digital Tokens (for example, bitcoin); only money will be accepted upon issuance. In order to cause Tether Tokens to be issued or redeemed directly by Tether, you must be a verified customer of Tether. No exceptions will be made to this provision. The right to have Tether Tokens redeemed or issued is a contractual right personal to you. Tether reserves the right to delay the redemption or withdrawal of Tether Tokens if such delay is necessitated by the illiquidity or unavailability or loss of any Reserves held by Tether to back the Tether Tokens, and Tether reserves the right to redeem Tether Tokens by in-kind redemptions of securities and other assets held in the Reserves. Tether makes no representations or warranties about whether Tether Tokens that may be traded on the Site may be traded on the Site at any point in the future, if at all.

[Excerpt from Terms of Service (Last updated: December 7, 2023) of Tether]

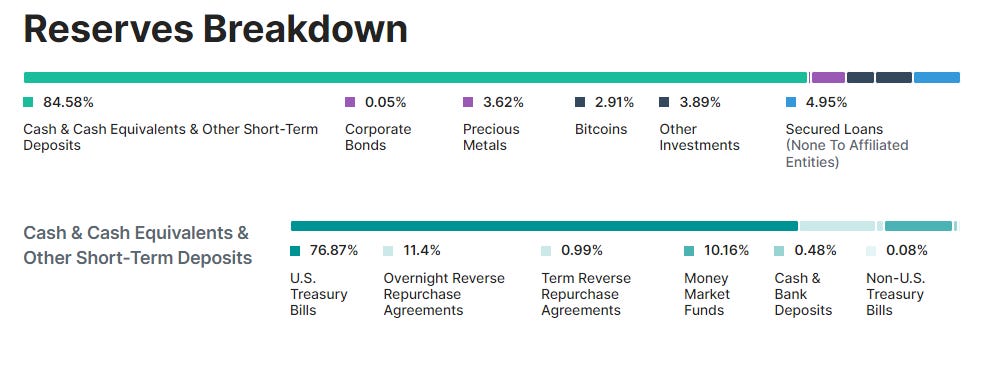

As of today, USDT reserves have been allocated to the following non-financial asset categories:

precious metals - 3.62%

bitcoin - 2.91%

other investments - 3.89%1

As a result, we can tell that a total of 10.42% of USDT reserves are comprised of non-financial assets. In total, 10.42% of USDT reserves comprise non-financial assets. However, precious metals and bitcoin, at least, are assets that are readily convertible to cash. The remainder of the assets, held in cash, cash equivalents, bonds, stocks, and secured loans, are typically viewed as financial instruments.

As a result, I assessed whether USDT is still appropriate to account as a financial asset in the same manner as USDC based on the following:

90% of USDT reserves are financial assets;

At least 6% of the remaining 10% of non-financial and potentially non-financial assets are readily convertible to cash assets;

Moreover, in practice, Tether has not exercised the right to settle USDT with the non-financial assets it holds in reserves.

Therefore, I believe that USDT should be accounted for as a financial asset.

It is not clear which items are included in the 'other investments' category; thus, we conservatively categorize this line item as potentially non-financial assets.