FASB Crypto Accounting Standard

Considerations related to the new FASB ASC 350-60 "Crypto Assets"

The Financial Accounting Standards Board (FASB) has recently introduced a standard on accounting for digital assets, significantly altering the landscape of crypto accounting and, finally, allowing the remeasurement of crypto assets at fair value. Let’s dive in on how the new FASB standard on digital assets is going to change the crypto accounting landscape.

#1 Remeasurements in the Absence of an Active Market

Under the new guidance, tokens lacking an active market are now subject to mandatory revaluation at the end of each reporting period [FASB ASC 350-60-35-1]. This significant shift likely necessitates the recurring involvement of valuation experts to employ Level 3 Fair Value measurement inputs for these tokens.

#2 Beware of Earnings Management Opportunities

Why are we talking about Earnings Management?

The ability to release unrealized gains on crypto assets into accounting results at management's discretion, by wrapping or unwrapping tokens (FASB ASC 350-60-15-1(a)), opens doors to earnings smoothing.

Businesses with fluctuating earnings are more likely to adopt fair value measurements and resort to such practices when earnings fall short of expectations.

Management can exploit this by accumulating unrealized gains and strategically recognizing them, particularly during periods of declining profits

It has been previously noted that businesses:

“with higher earnings volatility are more willing to adopt fair value measurement and tend to use fair values when earnings are less than expected”1

There are multiple ways to perpetrate this for different crypto asset ecosystems. For example, to create a cumulative reserve from unrealized gains on crypto assets in anticipation of the growing crypto market (in contrast to the company’s own declining operating results), management could accumulate unrealized gains on crypto assets and then need to recognize in the desired period by doing any of the following actions:

Invest in WETH, accumulate unrealized gains, and unwrap into ETH in a period of declining profits;

Invest in BTC and transfer assets to the lighting network account;

Invest in BTC and bridge assets in the Rootstock’s (RSK) 2-way peg protocol.

Case Study: BTC and RBTC Exchange

Let's examine a simplified example to illustrate these concerns.

On 1-1-2023, the Company P adopted ASC 350-60 effective 1-1-2023;

On 1-1-2024, P purchased 1 BTC for $20,000;

On 12/31/2024, the token price fell down to $14,000 and P recorded losses immediately;

On 1-1-2025, P bridged BTC to Rootstock’s ecosystem via the 2-way-peg (sent 1 BTC and received 1 RBTC - Rootstock’s Smart Bitcoin);

On 12-31-2025, the price on token increased up to $22,000 but no gains were recognized because RBTC is outside of the scope of ASC 350-60 and being accounted for under the historical costs less impairment model.

On 11-30-2026, the price on token increased up to $80,000 and P’s management noted that the unrealized gains they’ve accumulated on RBTC were significant enough to change the net loss to net profit position in the period. Therefore, they decide to bridge RBTC back on bitcoin mainnet network and benefit from recognizing the appeciation in the current period income in full. They sent 1 RBTC via the 2-way-peg and received 1 BTC.

On 12-31-2026, the price on token increased by another $3,000 and the gain was recorded on P’s books under ASC 350-60.

Below is an illustrative example with simplified numbers to explain this concern. Let’s assume that we have the following summary of relevant fair value (illustrative) data:

Excited with this opportunity, management transferred RBTC out of Rootstock’s ecosystem and exchanged it for BTC on the Bitcoin mainnet network. As BTC is in the scope of ASC 350-60, the company immediately recognized in 2026 the full amount of gains accumulated in the last two years.

As a result of this, the volatile and inconsistent trend in the net income turned out to be a 3-year straight 5% growth Year-over-Year (YoY):

On the chart below you can compare the YoY Growth that will be presented under ASC 350-60 to the same metrics that would be reported under the fair value accounting model applied for all assets:

It is obvious that the ability to recognize unrealized gains in an arbitrary period here without any substantive change in the financial position and results of the entity may misguide the investors. The new guidance introduced the opportunity to manipulate companies’ earnings which I think will not benefit neither users nor preparers of financial statements.

#3 Scoping for 100 Tokens

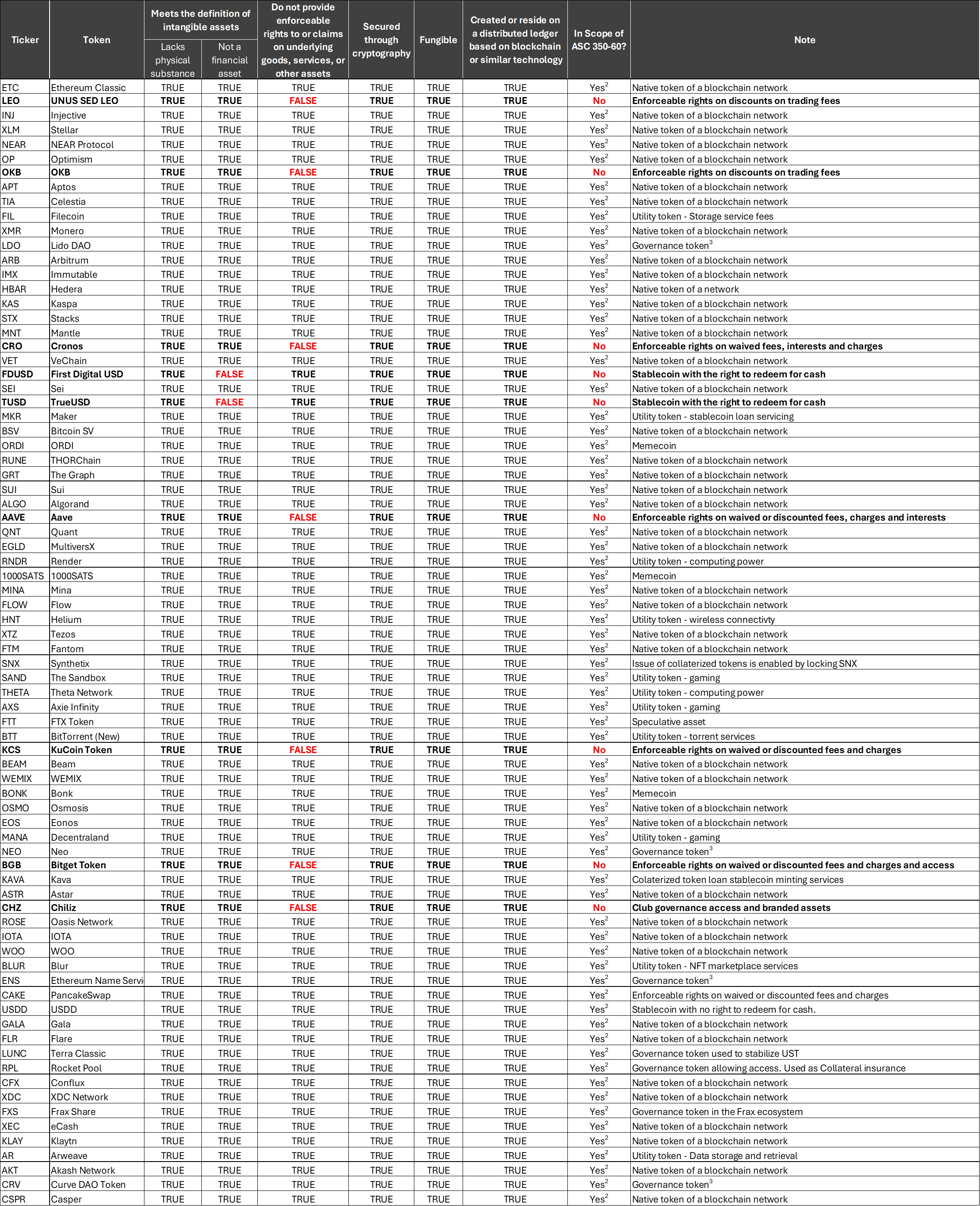

We analyzed all of the criteria listed in FASB ASC 350-60-15-1 to identify the scope of the new crypto asset accounting guidance for 100 tokens with the highest market capitalization as of the date this material was prepared.

We substituted the first criterion (a) with two sub-criteria derived from the definition of intangible assets - “Assets (not including financial assets) that lack physical substance. (The term intangible assets is used to refer to intangible assets other than goodwill.)” . This means that instead of verifying that the token “Meet the definition of intangible assets as defined in the Codification”, we used the following two criteria:

An asset lacks physical substance

An asset is not a financial asset

Criterion (b) “Do not provide the asset holder with enforceable rights to or claims on underlying goods, services, or other assets” poses a complex and judgmental question. To answer this question, we considered the fact that native tokens of blockchain networks almost always act as a medium of exchange and are required to pay for gas to execute blockchain transactions on the respective network. All such tokens can be viewed as providing enforceable rights for transaction validation service on this network. If we were to follow this interpretation, none of the main cryptocurrencies (BTC, ETH, etc.) would be in the scope of ASC 350-60. This would be non-productive to adopt this interpretation.

We noted that utility tokens provide holders with a certain ability to acquire goods, services, or assets. However, this ability is limited to the times when the holder has a sufficient amount of tokens to pay for the goods, services, or assets. Token holders have an option to purchase services and other assets using the token. But no claim on / enforceable right on the service or asset exists before such purchase. Hence, practically all utility tokens that we are aware of fall in the scope of ASC 350-60 because although underlying services or assets exist, no claim or right on these is granted to token holders by default.

Finally, Criterion (f) “Are not created or issued by the reporting entity or its related parties” was ignored here. Simply put, we assumed that the reporting entity is not affiliated with a token issuer. If this assumption is wrong, the conclusion will most likely be different.

In summary, we identified that the following from the 100 tokens we researched, the following categories comprised the tokens that are excluded from the scope of ASC 350-60:

Tokens that grant holders the right to use services at reduced or no cost (i.e. exchange tokens);

Stablecoins with the right of redemption for cash (should be accounted for as financial assets).

Details of our analysis for specific tokens are presented below. If you have a different opinion about the classification of any of the tokens listed here or would like to add other tokens to this list, please feel free to reach out to me at my email.

Yuanyuan Guo, Siqi Lu, Joshua Ronen, Jianfang (Jennifer) Ye (2022). Equity Financial Assets: A Tool for Earnings Management – A Case Study of the Youngor Group

Assumes that the reporting entity is not an issuer or related party of the issuer of tokens.

Although these tokens provide certain enforceable rights for community governance, these rights are not related to any specified good, service, or other asset. As such, we believe these tokens fall into the scope of the new accounting topic ASC 350-60.