FASB, FAF, AICPA, Antitrust Laws, and AI adoption by accounting firms

Let's talk about a legalized monopoly of FAF on the accounting and auditing standards market

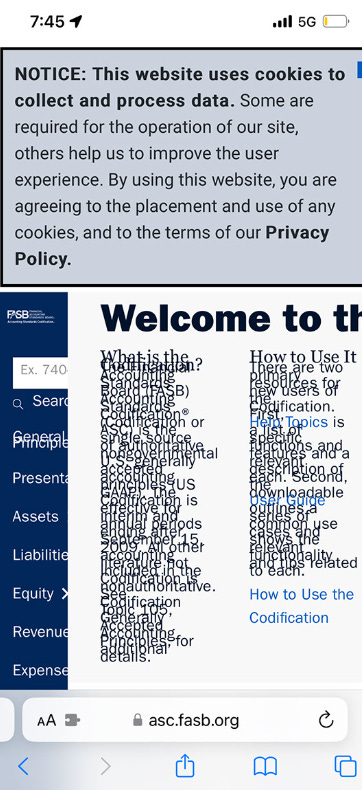

This morning, I tried to find something in the Accounting Standards Codification (FASB ASC) online. I didn’t have access to my laptop, so I typed `https://fasb.org` into the Safari browser on my iPhone. After a few clicks, I landed on the main page of the official online version of the FASB ASC. This is how it looks:

How helpful is it for accountants to have authoritative texts of accounting standards available for free in the format from the screenshot above? In my humble opinion, it is not very helpful. We need something different. Something better. Certainly, there are many solutions available out there, where you can easily access and search through FASB ASC. Or maybe not? Let’s find out and along the way discuss how privileges granted to FASB and actions they undertake define the accounting research industry today.

FASB is governed by FAF (Financial Accounting Foundation). Both FASB and FAF are private nonprofit organizations. FASB has exclusive right to adopt accounting standards that all domestic US public entities must comply with and that FASB itself follows.

Being a private organization, FAF is motivated to operate in a way that maximizes funding available to finance its operations. As a result, FAF acts in a way that prioritizes benefits received by this organization over benefits provided to the investors and accountants. Fortunately, FAF is a rightful owner of all intellectual property created by FASB (such as FASB ASC).

The U.S. Government has given FAF and AICPA unique monopolistic rights (on the authoritative texts of accounting and auditing standards, respectively). The organization leverage these rights to limit competition for companies they have a direct financial interest in. Private businesses cannot work with accounting and auditing standard texts without their permission.

In recent years, this feature of FASB has been criticized several times. We can find examples of this criticism in Harvard Law School Forum on Corporate Governance [1], Financial Times [2, 3], and publications of American Accounting Association [4]. But these issues were raised not only in media publications. In fact, most relevant to today’s discussion is a lawsuit raised back in 2010 against FASB for alleged violations of US antitrust laws.

Antitrust Laws

In 2010, FASB was sued for the violation of antitrust law after the board allegedly appropriated the patented intellectual property of Silicon Economics, Inc. (SEI). How did this happen? You see when a business submits any materials or ideas as part of the public meetings, comment process, or otherwise, FASB automatically is granted the intellectual property rights on such materials and ideas free of charge and can sell these materials and ideas to the external public for a price they deem appropriate. But does anyone care about nuances like this? What interests me more is that this case’s materials contained the first formulation of the understanding that our current accounting regulators act as a government-backed monopolies:

FASB controls over 90 percent of the market for “financial accounting standards in the United States”, and, as a result, that FASB is a “government-backed monopoly”.

FASB’s defense, in this case, included the following statement:

“Defendants argue they are not engaged in trade or commerce because their accounting standards are freely available to anyone in the world and are available without charge and without payment to Defendants, save for sales of bounded volumes and unrelated licensing arrangements.”

Now this contradicts the information presented in FAF financial statements:

“The FAF licenses the content of the FASB Accounting Standards Codification® (FASB Codification) to commercial publishers and others for inclusion in their proprietary, comprehensive, online research systems, and additional products.”

FAF Annual Report 2023

Further, based on the licensing terms FAF may terminate the right of any business entity to access and read (hence, follow) the accounting standards codification:

“6. Term and Termination…

(b) FAF may terminate this Agreement and Your right to receive the Codification and Related Content at any time without notice.

(c) Upon termination or expiration of this Agreement, all licenses granted under this Agreement shall cease and You shall immediately) cease access to and use of the Codification…”

However, these contradictions were not important to the court’s decision at that time. The case against FASB was dismissed due to the lack of jurisdiction, as FASB had no permanent presence in California where the other party resided.

Artificial Intelligence

Let’s fast forward to 2024.

I met with Peter Spencer, Director of Finance and Accounting at FAF on February 2, 2024, to learn that:

FAF sets prohibitively high fees for licensing the FASB ASC1

FAF rejects all applications for licensing the accounting standards codification from entities who intends to use these texts in generative AI applications.

The use of these texts was prohibited regardless of the application’s purpose, simply because FAF did not trust this technology and implemented a policy to deny licensing rights requests from anyone.

However, I learned that there is an exception made for several startups in which AICPA has had a direct ownership interest (for example, MateriaAI).

Current terms of service restrict the use of FASB ASC with AI as follows:

“(b) Artificial Intelligence. You may not use nor attempt to use any portion of the Codification (or as otherwise found on or accessed through the Codification site): (i) as input into or for the training or development of generative artificial intelligence, machine learning, algorithms, software, or related technologies, to create any derivative works, compilations or collective works; or (ii) for any purpose that: (A) infringes, misappropriates, or otherwise violates any intellectual property right of FAF or of any third parties which have licensed to FAF the right to redistribute or sublicense any materials, or (B) allows any third parties to access, use or benefit from our proprietary intellectual property in any way without specific permission from FAF to do so.

Accessing or using the Codification via mechanical, programmatic, robotic, scripted or any other automated means is strictly prohibited (including the use of automated systems or software to extract data from the Codification or the Codification website (‘screen scraping’)). Unless otherwise agreed to by FAF in writing, use of the Codification is permitted only via individual users engaged in an active user session and may not be collected via automated or robotic methods. Regardless of the data delivery method, neither the Codification website nor the Codification may be used in conjunction with a generative artificial intelligence (“AI”) solution. Portions of the Codification website may utilize – directly or indirectly - AI algorithms and technologies, including generative AI, to provide certain features. FAF may provide responsive or accelerated search results based on natural language queries or prompts that You provide while using the Codification. AI systems may not be accurate or error-free, which means You remain responsible for verifying any information provided on the Codification website. AI or use of the Codification or the related websites are not a substitute for professional advice.”

I agree that the use of generative artificial intelligence creates high risks when used without appropriate precautions. But I do also believe that it would be beneficial for us to have this issue solved by a free market of competing service providers. But it seems that on questions like these, FAF always takes a position prioritizing economic benefits of FAF over benefits provided to the public.

The short summary of everything we discussed above is:

FAF prohibits the use of texts of accounting standards to train AI models.

FAF set prohibitively high fees for licensing of FASB ASC that prevent new businesses from entering the market.

FAF denies licensing applications from any software development businesses that attempt to use authoritative texts with applications using generative AI.

…with an exception made for companies in which the AICPA has a direct investment stake.

Conclusion

FAF owns the Accounting Standards Codification (FASB ASC), the only set of accounting standards with an authoritative status for domestic public companies in the US. It is argued that FAF is a government created monopoly that prevents competition in our industry.

FAF and FASB actively defend their economic interests in courts. But these organizations have no economic interest or motivation to release robust, consistent, fault-tolerant, and detailed guidance. No other organization has the right to issue faster or better accounting standards with authoritative status.

Access to authoritative accounting standards is difficult. Accountants should work hard to find relevant pieces of accounting standards. As a result, standards grow in complexity, inconsistency, and rudimentary provisions, while the collective knowledge of these standards declines.

It is my understanding that the purpose of this is to prevent new businesses from entering the market.

Yet analysts often scrape the 10-ks, many of which discuss accounting standards at length, to train AI models. Is that a violation of any laws or agreements?